Budgeting for Millennials: Smart Money Habits for Success

Understanding the Importance of Budgeting

Why is budgeting crucial for millennials?

Budgeting is essential for millennials for several reasons:

- Financial awareness: It helps them understand their income and expenses clearly.

- Debt management: Many millennials face student loan debt; budgeting helps manage and pay off debts efficiently.

- Goal setting: It allows for planning major life events like buying a home or starting a business.

- Building savings: Regular budgeting encourages saving for emergencies and future needs.

- Retirement planning: Starting early with retirement savings through budgeting can lead to long-term financial security.

What are the common financial challenges faced by millennials?

Common financial challenges faced by millennials are:

- Student loan debt: Many millennials start their careers with significant educational debt.

- Rising living costs: Housing, healthcare, and other essentials are often more expensive relative to income.

- Stagnant wages: In many sectors, wages haven’t kept pace with inflation or living costs.

- Gig economy instability: Many millennials work in less stable, contract-based jobs.

- Delayed milestones: Financial pressures often lead to postponing major life events like marriage or homeownership.

- Technology and lifestyle inflation: Constant exposure to new products and experiences can lead to overspending.

How can effective budgeting lead to financial freedom?

How effective budgeting can lead to financial freedom:

- Debt reduction: Consistent budgeting helps allocate more funds to paying off debts faster.

- Increased savings: Regular savings, even small amounts, can grow significantly over time.

- Informed decision-making: Understanding your finances leads to smarter spending and investing choices.

- Goal achievement: Budgeting helps prioritize and save for important life goals.

- Stress reduction: Financial clarity reduces anxiety about money matters.

- Investment opportunities: With proper budgeting, excess funds can be invested for future growth.

- Flexibility: A solid financial foundation provides more career and lifestyle choices.

Creating a Budget: Where Do You Start?

Creating a budget is an essential step toward financial control. Let’s break down the process and explore some effective methods:

What are the first steps in creating a budget?

Gather financial documents: Collect bank statements, pay stubs, bills, and receipts.

Choose a budgeting tool: Decide between apps, spreadsheets, or pen and paper.

Determine your budgeting period: Monthly is common, but choose what works for you.

Set financial goals: Identify short-term and long-term objectives to guide your budget.

How do you assess your income and expenses?

Income assessment:

- List all sources of income (salary, freelance work, investments, etc.)

- Calculate your total monthly income after taxes

Expense assessment:

- Track all expenses for a month

- Categorize expenses (e.g., housing, food, transportation, entertainment)

- Distinguish between fixed and variable expenses

- Identify non-essential spending

What budgeting methods work best for millennials?

Budgeting methods that work well for millennials:

a) 50/30/20 Rule:

- 50% for needs (rent, groceries, utilities)

- 30% for wants (entertainment, dining out)

- 20% for savings and debt repayment

b) Zero-Based Budgeting: Allocate every dollar of income to a specific expense or savings category, so income minus expenses equals zero.

c) Envelope System: Allocate cash for different expense categories in separate envelopes. When an envelope is empty, stop spending in that category.

d) Pay Yourself First: Automatically transfer a set amount to a savings account before budgeting the rest.

e) Values-Based Budgeting: Align spending with personal values and long-term goals.

Essential Budgeting Tools and Apps

Technology has revolutionized personal finance management, making budgeting more accessible and convenient. Let’s explore some of the best budgeting tools and apps, including printable options, and how they can simplify the budgeting process.

What are the best budgeting apps available today?

Best budgeting apps available today:

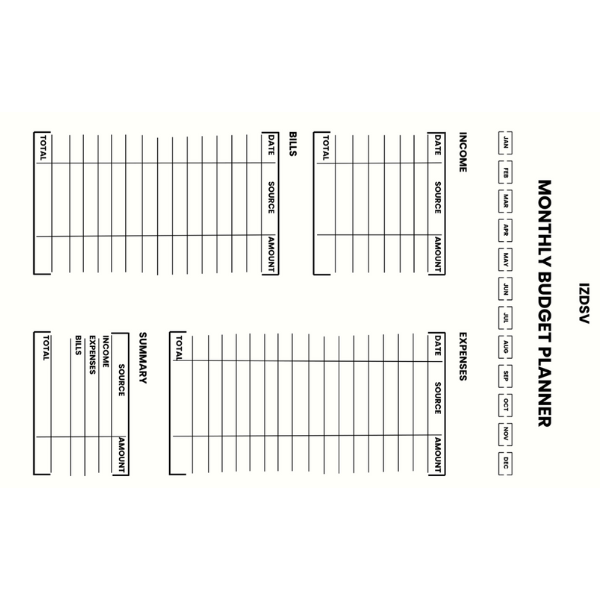

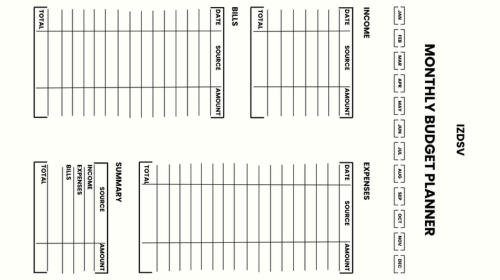

- Printable budget planner: Similar to a financial planner, but often more focused on day-to-day expense tracking and monthly budgeting.

- Mint: Free app that automatically categorizes transactions and provides a comprehensive overview of your finances.

- YNAB (You Need A Budget): Focuses on giving every dollar a job, encouraging proactive money management.

- Personal Capital: Combines budgeting with investment tracking, ideal for those looking to manage their overall financial picture.

- PocketGuard: Simplifies budgeting by showing how much you have left to spend after accounting for bills and savings goals.

- Goodbudget: Uses the envelope budgeting system in a digital format.

- Printable financial planner: While not an app, many people prefer the tactile experience of a physical planner. These often include sections for tracking expenses, setting goals, and monitoring debt payoff.

How can technology simplify the budgeting process?

How technology simplifies the budgeting process:

- Automatic transaction categorization: Many apps can categorize your spending automatically, saving time and providing insights into spending patterns.

- Real-time updates: See your current financial status anytime, anywhere.

- Bill reminders: Never miss a payment with automated alerts.

- Goal tracking: Set and monitor progress towards financial goals visually.

- Syncing across devices: Access your budget from your phone, tablet, or computer.

- Report generation: Easily create and analyze spending reports.

- Integration with financial institutions: Automatically import transactions from your bank and credit card accounts.

- Customizable categories: Tailor expense categories to your specific needs.

Incorporating printable options:

While digital tools offer many advantages, printable financial planners and budget planners remain popular for several reasons:

- Tangibility: Some people find physically writing down expenses more impactful.

- No screen time: Provides a break from digital devices.

- Customization: Easily modify layouts to suit personal preferences.

- Visual reminder: Having a physical planner visible can serve as a constant reminder of financial goals.

- Privacy: Some prefer not to have their financial data stored digitally.

The best budgeting method is the one you’ll consistently use. Experiment with different tools and techniques to find what works best for you.

Common Budgeting Mistakes to Avoid

What are the top budgeting pitfalls for millennials?

Top budgeting pitfalls for millennials:

- Underestimating expenses: Many millennials fail to account for all their spending, especially small, frequent purchases.

- Ignoring irregular expenses: Forgetting to budget for annual costs like insurance premiums or car maintenance can derail your finances.

- Setting unrealistic goals: Trying to cut expenses too drastically can lead to frustration and abandonment of the budget.

- Not having an emergency fund: Failing to save for unexpected expenses can lead to debt when emergencies arise.

- Lifestyle inflation: As income increases, allowing expenses to rise proportionally without increasing savings.

- Neglecting to update the budget: Not adjusting the budget as circumstances change can make it irrelevant.

- Forgetting about savings and investments: Treating savings as an afterthought rather than a priority.

- Using credit cards irresponsibly: Relying on credit cards to cover shortfalls without a plan to pay them off.

How can you stay motivated to stick to your budget?

Here’s how to stay motivated to stick to your budget:

- Set clear, achievable goals: Having specific financial objectives gives your budget purpose.

- Celebrate small wins: Acknowledge when you meet budget targets, even minor ones.

- Visualize progress: Use charts or graphs to see how you’re advancing towards your goals.

- Find an accountability partner: Share your goals with a friend or family member who can offer support.

- Use apps with gamification features: Some budgeting apps turn financial management into a game-like experience.

- Reward yourself: Plan small treats when you hit major milestones.

- Focus on the positive: Think about what you’re gaining (financial freedom) rather than what you’re giving up.

- Automate where possible: Set up automatic transfers to savings to reduce the temptation to overspend.

What should you do if you go over budget?

Don’t panic: Going over budget occasionally is normal. The key is how you respond.

Analyze the overspending: Determine if it was a one-time expense or a recurring issue.

Adjust your budget: If the overspending was due to an unrealistic budget, revise it to be more achievable.

Cut back in other areas: Look for ways to reduce spending in other categories to balance out the overage.

Avoid the credit trap: Try not to rely on credit cards to cover budget shortfalls.

Plan for future irregular expenses: If the overage was due to an unexpected cost, incorporate similar expenses into future budgets.

Use it as a learning experience: Reflect on what led to overspending and how you can prevent it in the future.

Consider using a buffer: Some people find it helpful to include a small “miscellaneous” category in their budget for unexpected expenses.

The key to successful budgeting is consistency and adaptability. Use tools like this printable planner alongside your chosen budgeting method, whether it’s an app, spreadsheet, or traditional pen-and-paper approach. Regularly review and adjust your budget as needed, and don’t be discouraged by occasional setbacks. Each month is a new opportunity to improve your financial habits.

Saving and Investing: What’s the Connection?

Budgeting, saving, and investing are interconnected aspects of financial planning that work together to build long-term wealth. Let’s explore how budgeting can facilitate saving and how millennials can approach both saving and investing effectively.

How can budgeting help with saving for the future?

How budgeting helps with saving for the future:

- Identifying excess income: A well-crafted budget helps you see where your money is going and identify areas where you can cut back to increase savings.

- Prioritizing savings: By including savings as a line item in your budget, you treat it as a non-negotiable expense rather than an afterthought.

- Setting specific goals: Budgeting allows you to set concrete savings targets and track progress towards them.

- Reducing impulse spending: When you have a clear budget, you’re less likely to make unplanned purchases that could otherwise go towards savings.

- Creating financial awareness: Regular budgeting increases your overall financial consciousness, often leading to more mindful spending money and saving money.

What are some effective saving strategies for millennials?

Some of the effective saving strategies for millennials are:

- Pay yourself first: Automatically transfer a portion of your income to savings as soon as you get paid.

- Use the 50/30/20 rule: Allocate 50% of income to needs, 30% to wants, and 20% to savings and debt repayment.

- Challenge yourself: Try no-spend days or months to boost savings and spending habits.

- Leverage technology: Use apps that round up purchases and help you save the difference or automatically transfer small amounts daily.

- Build an emergency fund: Aim for 3-6 months of living expenses in an easily accessible account.

- Take advantage of employer matches: If your company offers a 401(k) match, try to contribute enough to get the full match – it’s essentially free money.

- Consider high-yield savings accounts: These often offer better interest rates than traditional savings accounts.

- Set up multiple savings accounts: Create separate accounts for different goals (e.g., emergency fund, vacation, down payment) to track progress more easily.

How should millennials approach investing within their budget?

How millennials should approach investing within their budget:

- Start early: Even small amounts invested now can grow significantly over time due to compound interest.

- Educate yourself: Before investing, learn about different investment vehicles, risk tolerance, and basic investment strategies.

- Consider low-cost index funds: These provide broad market exposure with lower fees than actively managed funds.

- Use tax-advantaged accounts: Maximize contributions to accounts like 401(k)s and IRAs for potential tax benefits.

- Diversify: Spread investments across different asset classes to manage risk.

- Automate investments: Set up automatic transfers to investment accounts to ensure consistent investing.

- Rebalance regularly: Periodically adjust your investment mix to maintain your desired asset allocation.

- Be cautious with trends: Avoid jumping into investment fads without thorough research.

- Don’t neglect other financial priorities: Balance investing with paying off high-interest debt and maintaining an emergency fund.

Long-term Financial Goals: How Do You Plan for Them?

Long-term financial planning is crucial for millennials to secure their financial future.

What long-term financial goals should millennials consider?

Long-term financial goals millennials should consider:

- Retirement savings: Start early to take advantage of compound interest.

- Homeownership: Save for a down payment if owning a home is a goal.

- Debt elimination: Pay off student loans and other long-term debts.

- Career development: Invest in education or skills to increase earning potential.

- Building wealth: Create an investment portfolio for long-term growth.

- Family planning: Save for future children’s education or starting a family.

- Business ventures: Save capital for entrepreneurial pursuits.

- Financial independence: Work towards having the option to retire early or change careers.

How can budgeting help achieve these goals?

Budgeting can help achieve these goals by:

- Goal prioritization: Budgeting forces you to rank your financial goals and allocate resources accordingly.

- Consistent progress: By including goal-specific savings in your monthly budget, you ensure steady progress.

- Reality check: A budget helps you understand if your goals are realistic given your current financial situation.

- Accountability: Regular budget reviews keep you accountable to your long-term objectives.

- Flexibility: As circumstances change, budgeting allows you to adjust your financial plan while keeping sight of long-term goals.

- Visualizing trade-offs: Budgeting helps you see how current spending impacts long-term goal achievement.

- Identifying opportunities: Through budgeting, you might find areas where you can cut back to allocate more towards long-term goals.

What role does an emergency fund play in long-term planning?

The role of an emergency fund in long-term planning can be:

- Financial buffer: Protects your long-term investments from unexpected short-term needs.

- Reduces reliance on debt: Prevents the need to use high-interest credit cards or loans for emergencies.

- Provides peace of mind: Knowing you have a safety net allows you to focus on long-term planning.

- Maintains momentum: Helps you stay on track with long-term goals even when unexpected expenses arise.

- Increases financial flexibility: Allows you to take calculated risks (like changing careers) that align with long-term goals.

- Prevents early withdrawal penalties: Keeps you from tapping into retirement accounts prematurely.